Challenges and Opportunities in Developing Viable Business Cases for Digital Financial Services in the Refugee Context

Summary

World Food Programme (WFP) and the United Nations High Commission for Refugees (UNHCR) made a strategic decision, driven by the increasing cost of delivering food and material aid, to transition from material aid support to refugees to cash-based transfers.

This insight was developed from a UNCDF/DanChurchAid project that involved mapping the Digital Financial Services (DFS ) ecosystem in BidiBidi Refugee Settlement and developing viable business cases to support cash-based interventions. This was carried out between January and May 2018.

This insight does not represent the entire scope of the project. Rather, it focuses on the main challenges and opportunities that ought to be considered when developing DFS business cases in the refugee context, with Bidi Bidi as a case study.

Overview

Digital Financial Services (DFS) refer to the use of digital channels such as mobile phones, cards, computers, and tablets to deliver financial services. In Uganda, the term Mobile Money is widely associated with DFS because of wide usage of mobile phones to access various financial services offered on the mobile money platform. Mobile money particularly plays a very big role in enhancing financial inclusion in refugee settlements.

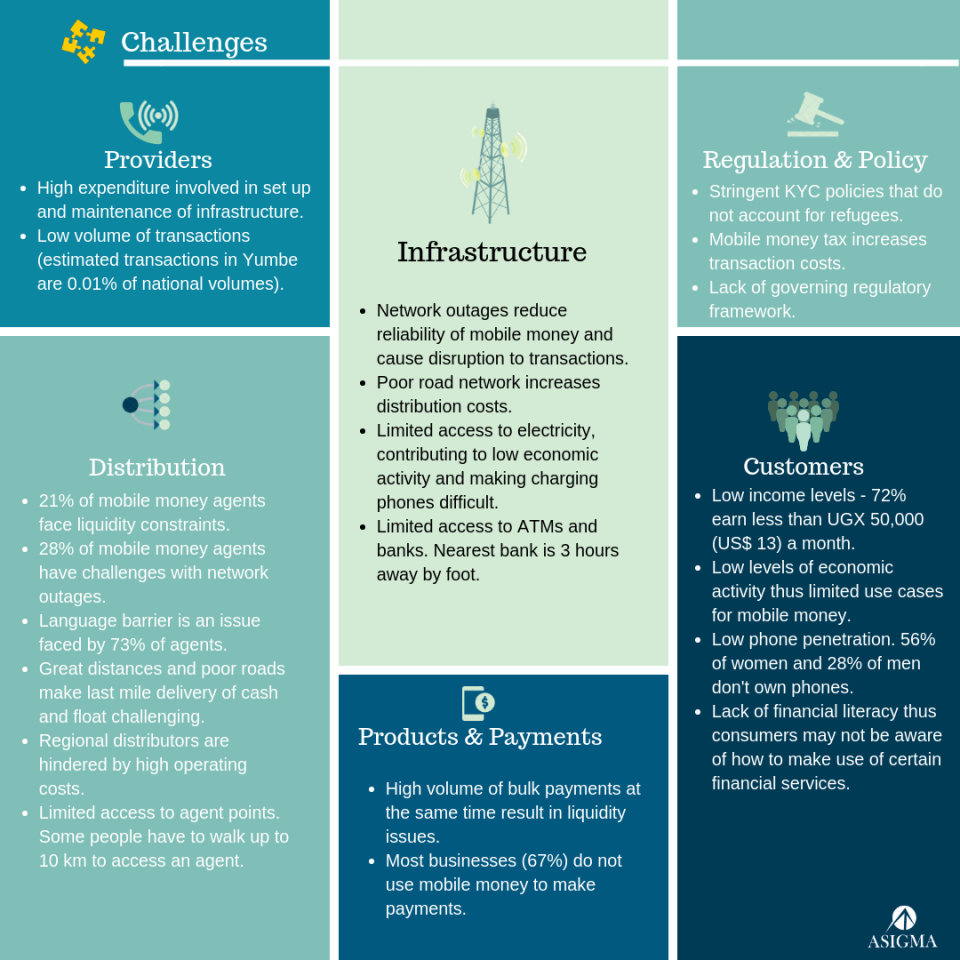

A DFS ecosystem involves the regulatory and policy framework governing the ecosystem, the infrastructure that supports the services, customers that use the services, the products and payments availed to customers, the distribution network through which customers are reached, and the providers of DFS. Each component of the ecosystem is necessary for successful uptake of DFS services and successful business cases that results in profitability for service providers.

Challenges

The refugee context presents several challenges with regard to various aspects of the DFS ecosystem. Below is a summary of factors inhibiting use of DFS among refugees in Bidibidi.

Opportunities

Despite the challenges faced, several players are identifying opportunities to invest in the development of a DFS ecosystem both for humanitarian and profit goals.

Further Considerations

In a broad sense, a business case is developed prior to the investment decision. The following sub section examines deliberations that must be considered when developing viable business cases for mobile financial services in refugee settlements.

1. Growth in Mobile Money Transactions

As a result of the large capital and operating costs, there is need for high volume of activity in order for it to be profitable for MNOs and aggregators to operate in a specific area. To support the business case for offering digital financial services to refugees in Bidibidi initially, there is need for development agencies to channel a large portion of the cash transfers through mobile money.

Payments from development agencies are however likely to decline year on year as the situation stabilises in countries of origin. This raises a sustainability issue and calls for growth in mobile money usage to occur simultaneously. Growth in transaction volumes requires efforts to increase economic activities through improvement in livelihood and market systems. This enhances sustainability and reduces dependence on humanitarian payments to support the mobile money ecosystem.

2. Financial Literacy Training

To boost the demand side, there is also need for mobile and financial literacy training in order to enhance customers’ ability to make informed decisions about money management. This will boost use of both traditional mobile money functions such as cash-in and cash-out transactions as well as other products such as savings and credit.

3. Products Tailored to Market

Providers should offer products tailored to these markets. For instance, ASIGMA’s research in Bidibidi found that about half (49%) of people are part of a SACCO or VSLA. These groups are willing to adopt the use of mobile phones for group activities, however they are limited by cost of mobile phones, transaction costs and access to agents.

Whilst refugees are perceived as risky segment for credit products, Kiva a not-for-profit organisation has been lending to refugees through the World Refugee Fund (WRF) and found that “Loans to refugees and IDPs have a repayment rate on Kiva of 96.6%, versus 96.8% for all non-refugee loans during the same period.” This indicates that there could be some credit worthy clients within refugee populations.

4. Distribution Network

Mobile Network Operators have to invest in setting up an adequate distribution network. An inadequate distribution network reduces reliability of mobile money services and results in users withdrawing their accounts entirely when money is received since access to agents is limited.

MNO’s in the area typically outsource last mile delivery to other companies (distributor), the distributors however face challenges with liquidity management, language barriers and high operating costs. Distributors in Bidibidi travel to agent points providing them with e-value or cash, this results in high transport and personnel costs. It is therefore important for remuneration structures to adequately incentivise the distributor to build a reliable distribution network.

5. Innovative Business Models

Providers need to make use of innovative models to tackle some of the challenges faced and enhance sustainability of business cases developed. Predictive data analysis can be used to better manage agent liquidity this is enabled through use of Management Information Systems (MIS). Use of an MIS also allows aggregator offer credit services to agents for working capital, based on their performance.

Another model is to leverage the distribution network built to offer bundled services or products. This creates a better value proposition for agents recruited as they are not solely dependent on mobile money revenues. This can be through offering bundled service through innovations such as solar powered kiosks which offer mobile phone charging services, a service in demand in rural areas due to limited access to electricity. GSMA anticipates that in the future, agent networks will be offered to banks, fintechs and insurance companies as a service. In this way the mobile money agent functions as a one stop service. They also find that agent distribution networks can be useful in tackling challenges e-commerce providers face with delivery whilst providing agents with higher income.

Conclusion

There are several stakeholders operating in the ecosystem. These include Regulatory Bodies, Humanitarian Agencies, Government, Mobile Network Providers, Private Sector Players and Aggregators. Developing a viable business case entails having to assess not only the roles that these different groups play but also what they have to do in order for the business case to work.

There is need for an enabling regulatory framework in order for the ecosystem to develop with consideration for refugee and other segments of the un-banked population. Humanitarian agencies need to continually support livelihood development in order to boost economic activity that can sustain mobile money ecosystem without dependence on payments from development agencies. Mobile Network Providers and other private sector players need to look into innovative business models and partnerships that can enhance viability and sustainability whilst operating in such areas.

By looking at the DFS ecosystem holistically, a viable business case can be developed even in difficult environments such as Bidibidi. However, due to the underdeveloped nature, the business case must be supported by interventions by various stakeholders to ensure an enabling environment.

Download the full report from ReliefWeb for more information.

This insight is not paid research but rather internal research based on our advisory and data projects. It is being shared to create public debate and, as such, we welcome any suggestions for improvement. Kindly contact us at info@asigmacapital.com