Micro and Small Enterprises (MSEs) Financing in Uganda An Insight on the Financing Gap for MSEs in Uganda

Introduction

ASIGMA is presently engaged in a 5-year initiative focused on facilitating financial access to the MSE (Micro and Small Enterprises) segment through Tier III and IV Financial Institutions. Through extensive collaboration with more than 50 Tier III & IV Financial Institutions and the indirect extension of credit to over 48,000 MSEs, ASIGMA has accumulated substantial data. This data has been meticulously analysed to extract valuable insights and key learnings that can be leveraged to enhance access to finance for the MSE segment.

Summary

Micro and Small Enterprises (MSEs) are considered a marginalised economic segment regarding access to finance despite accounting for 90% of the private sector and producing over 80% of output and 75% of the country’s GDP.

Key Pointers

- MSEs are normally sole proprietorships that cannot be disassociated from their owners.

- MSE owners are categorised as high-risk clients by most of the Financial Institutions which hinders their access to finance.

- The elevated risk associated with MSEs can be attributed to factors such as their volatile income streams, frequent mobility, borrower non-compliance and the absence of collateral.

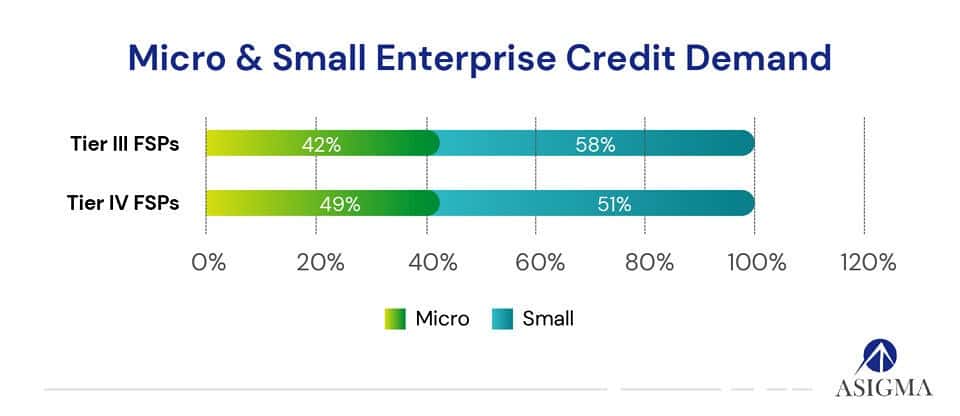

- Micro and Small Enterprises have an almost equal share in demand capacity from Tier III FIs while the Small Enterprises slightly lead the Micro Enterprises when borrowing from Tier IVs contrasting popular belief that the small enterprise segment has far greater credit demands that outstrip the demand of the micro-enterprise segment.

- In terms of demand capacity from Tier III FIs, Micro and Small Enterprises exhibit nearly equal shares. However, Small Enterprises hold a slight lead over Micro Enterprises when seeking loans from Tier IVs.

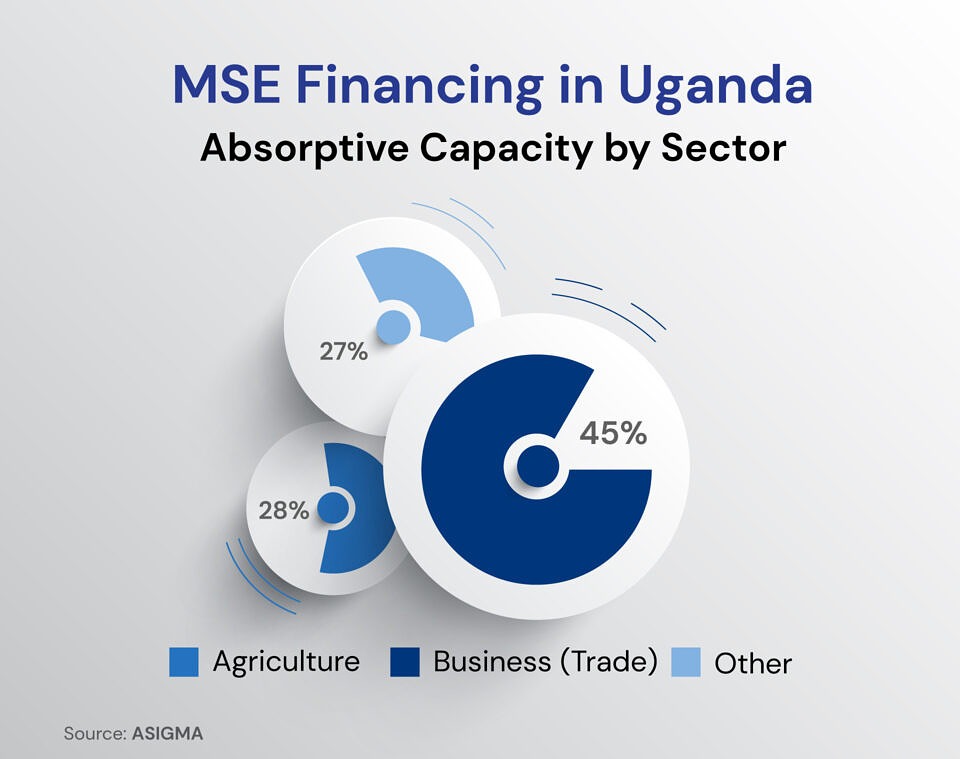

- Agriculture and business have the highest are the highest absorbing sectors of the MSE credit at 27% and 45% respectively.

- The average loan ticket size for MSEs is UGX 1.4 M.2

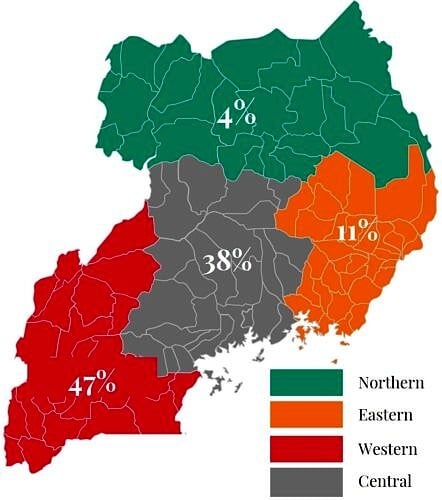

- The predominant demand for and access to credit by MSEs is concentrated in Central and Western Uganda, representing a collective 85% of MSEs.

This insight delves into a market system perspective, that examines the dynamics between demand and supply while emphasising the enablers, impediments and possible interventions.

The Demand Side

The composition of the demand side is mainly small-scale enterprises not limited to but including retail and wholesale businesses, farmers, cooperatives, microfinance institutions, construction and manufacturing businesses.

The estimated demand for credit by the sector in Uganda is approximately UGX 31.4 trillion ($8.8 billion).

The predominant demand for and access to credit by MSEs is concentrated in Central and Western Uganda, representing a collective 85% of MSEs as per the ASIGMA Data Analytics. This trend is propelled by the substantial presence of SACCOs in Western Uganda and Tier IIIs in the Central region, fostering a conducive supply environment. Additionally, the heightened productivity in these areas, particularly in agriculture and trade, serves as a driving force for increased credit absorption.

The economic vitality of these regions is underscored by Uganda’s poverty map. Consequently, the Northern and Eastern regions face challenges in attracting financial service providers due to lower demand for such services in these areas.

Geographical Spread of MSE Credit

Source: Asigma Capital Data Analytics

In terms of credit demand, the Micro and Small Enterprises an almost equal share in demand capacity from Tier III FIs while the Small Enterprises lead the Micro Enterprises when borrowing from Tier IVs as Illustrated below.

This contrasts with the popular belief that the small enterprise segment has far greater credit demands that outstrip the demand of the micro-enterprise segment.

Lending to the Women and Youth

In the realm of MSEs’ access to finance, women and youth continue to face marginalisation, encountering challenges in meeting lender requirements, particularly regarding collateral such as land and other traditional collateral, which often remain under the custody of non-youth men. Numerous initiatives with Financial Service Providers (FSPs) have collaboratively emerged to enhance financial inclusion for women and youth. The tide is beginning to shift, with positive changes and growth underway.

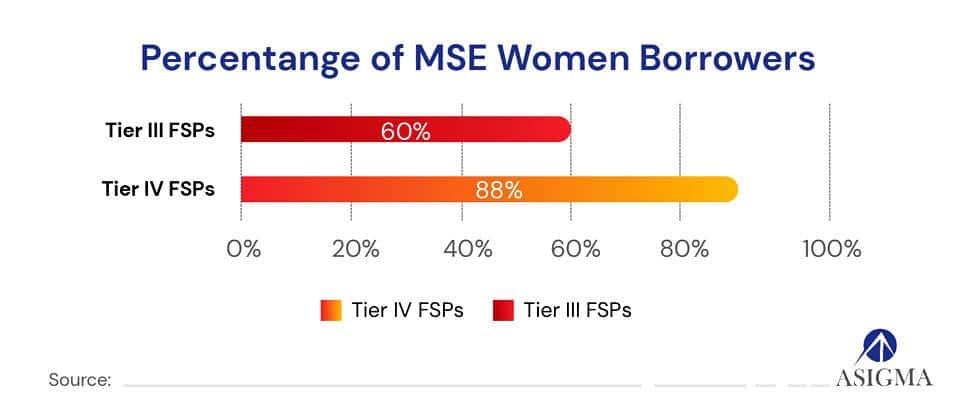

In the ongoing 5-year initiative focused on providing access to finance for women and youth, it has been discovered that more women are borrowing from Tier IVs than Tier IIIs. Tier IVs successfully attract female MSE borrowers through group loan* products, eliminating the necessity for physical or movable collateral. Instead, these loans rely on social guarantees and Know Your Customer (KYC) processes for debt access. Due to stringent regulatory requirements set by the central bank to maintain a healthy portfolio, and in some instances, the Tier IIIs’ aspirations to advance to higher Tiers, their risk appetite for serving MSEs diminishes over time. This reduction in risk appetite affects their ability to cater to high-risk clients, such as women without collateral.

* Group Loans are money loans to a group of people through a microfinance institution or SACCO, normally characterised by small ticket sizes and short tenors and rely on social guarantees as a form of collateral or security.

Challenges facing MSE Financing

The credit gap is the biggest challenge facing MSEs in Uganda. The primary concerns revolve around the accessibility of financial resources and the availability of pertinent information for businesses of this nature. Most of these businesses are considered ineligible for traditional credit services, making them unable to secure funding for their operations.

Leveraging our experience and close collaboration with MSEs, we have identified critical issues impacting the performance of these businesses within Uganda’s current economic climate. The key issues include:

- Access to Finance/Capital: Micro and Small Enterprises (MSEs) face challenges in accessing financing from traditional Financial Service Providers (FSPs) such as banks, primarily due to stringent eligibility criteria that extend beyond just interest rates. Consequently, MSEs have turned to alternative sources like moneylenders or informal lending channels to fulfill their business funding requirements.

- Lack of Collateral: Micro and small enterprises (MSEs) often find themselves without the necessary traditional collateral to fulfil the demands of traditional lending standards, which typically stipulate assets such as equipment, land, and buildings. Frequently, MSEs depend on personal guarantors who often share a similar informal status as the loan applicant, thereby limiting their ability to secure loans.

- Policy and Regulatory Constraints: The intricate nature of regulations and policies in taxation, trade, and licensing, compounded by low literacy levels among those in the informal sector, creates significant hurdles for MSEs. It obstructs their capacity to fulfill prerequisites, generate necessary documentation, and consequently restricts their access to formal financial services while impeding their ability to comply with legal standards.

- Skills Gap and Training: The lack of necessary skills and managerial expertise in MSEs makes them appear less capable of effectively managing funds, reducing their creditworthiness, and increasing the perceived risk for lenders.

- Inadequate Financial Documentation: MSEs often lack comprehensive financial documentation and statements that meet the criteria set by lenders. Insufficient financial records, audited statements, or dependable financial forecasts impede their capacity to obtain financing.

- Limited Investor Awareness: MSEs frequently face difficulties in capturing the interest of potential investors. Venture capitalists, angel investors, and other investment firms might predominantly concentrate on more substantial investments or possess limited insight into the potential offered by SMEs. This limited awareness can create obstacles for SMEs in identifying suitable investors.

The Supply Function

Approximately half of the financial requirements of businesses falling under the MSE segment are fulfilled by Tier III and IV Financial Institutions. Tier III FIs and SACCOs with more than UGX 1.5 B in savings are regulated by the Central Bank of Uganda. The Tier III FIs include Deposit-taking Taking Microfinance Institutions (MFIs). Tier IV institutions consist of Non-Deposit Taking MFIs, Savings and Credit Cooperative Organisations (SACCOs), Money Lenders, and Fintech companies, all of which offer lending services.

Given the nature of MSEs, these enterprises usually seek smaller loans, typically ranging from UGX 100,000 to 10 million, with shorter repayment periods spanning from 1 month to 2 years. This contrasts with the usual clientele of Tier I and II commercial banks.

Tier III & IV Financial institutions have strategically situated themselves to meet the needs of MSEs and to address the specific traits of financing tailored for MSEs by:

- Proximity to customers: Tier III and IV FIs deliberately target MSEs and have established a broad geographical presence to address the credit needs of local MSE populations, akin to how the SACCO model operates.

- Tailored products: They offer customised products to address MSE needs, including emergency loans, solar loans, and specialised offerings like “boda boda loans,” which have gained popularity. Additionally, they provide business loans with flexible terms.

- Simplified interest rate pricing: FSPs targeting MSEs tend to price their loan products monthly due to the short-term nature and tenor of these loans.

- Customer-centric services: MSEs prefer personalised, relationship-based customer experiences, where they are guided through the loan application process and even during recovery.

- Leveraging Technology: These FIs employ Loan Management Systems to efficiently handle a large customer base. They also utilise digital mobile platforms, including USSD codes and mobile applications, to streamline service delivery to customers dispersed across rural areas. This approach has reduced the need for an extensive branch network in areas where a smaller customer base cannot cover branch operational costs.

Challenges faced by MSE FSPs

- High cost of external debt: Access to affordable debt is crucial for FIs, but Tier III and IV institutions find it challenging to secure cheap debt due to less stringent regulations at lower tiers and their unique customer base. Unlike Tier I and II FSPs that often rely on debt at single-digit interest rates from foreign parent companies and substantial deposits to finance their loan portfolios, Tier III & IVs, for example, experience an average cost of debt exceeding 16%.

- MSEs are normally sole proprietorships, and the borrowers cannot be disassociated from the business. MSE borrowers for example boda bodas are sometimes very mobile without a permanent address which makes it hard for the FSPs to monitor and recover debt in case of borrower indiscipline.

- Unstable Incomes of MSEs: Predicting the earnings and cash flows of MSEs during loan appraisal is a recurring challenge, often resulting in higher loan amounts approved than can be repaid. Informal MSE businesses, coupled with erratic income streams and inadequate record-keeping, contribute to borrowers defaulting on payments.

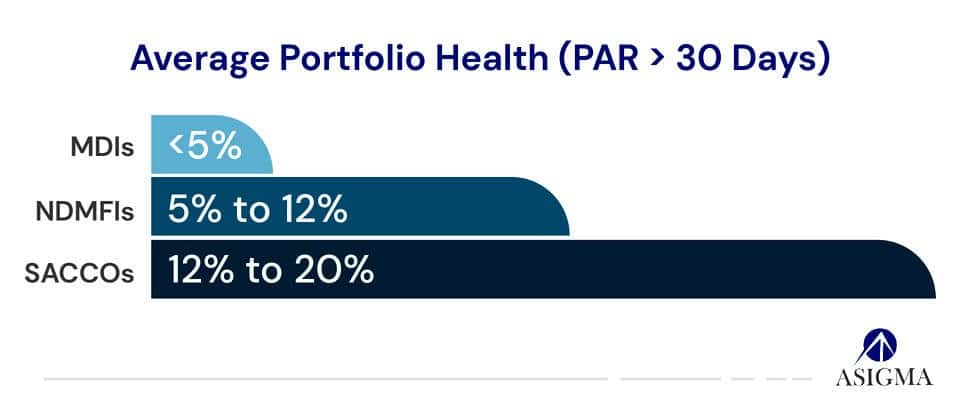

- High Portfolios at Risk (PAR): Due to unstable incomes and borrower indiscipline among MSEs, FSPs targeting this segment often experience high PAR, exceeding 30 days which surpasses 15% in some cases. This issue is particularly common among Tier IV FSPs, where the MSE segment constitutes over 60% of their customer base. The high PAR can deter investors and external lenders, leading to elevated external debt costs.

- Limited adoption of credit reference services: Tier IV FSPs encounter difficulties in implementing credit referencing services compared to BOU-regulated Tier I, II, and III institutions. Given the already high cost of credit products for MSEs, FSPs struggle to incorporate the additional cost of credit referencing, particularly when dealing with small loan amounts which is what most MSE borrowers seek. The average cost of obtaining a CRB report is UGX 15,000 which when compared to the average ticket size of UGX 1.4M translates to a 1% increment in borrowing fees.

- Infrastructure challenges: Inadequate branch networks and transportation options make it challenging to meet the needs of MSEs and monitor loans. This issue is particularly pronounced in very rural and peri-urban regions of Uganda.

Interventions

In addressing the critical challenges faced by MSEs in Uganda regarding access to finance, a comprehensive and multi-dimensional approach is essential. Implementing targeted strategies tailored to the specific needs of MSEs can pave the way for enhanced financial inclusion, sustainable growth, and economic resilience within this vital sector.

Each actor has a unique role to play in addressing MSE financing challenges in Uganda. Collaboration and coordination among these stakeholders are critical to implementing effective and sustainable solutions that can significantly improve financial access and support for MSEs in the country. These stakeholders include Financial Institutions, Government and Regulatory bodies and Development Partners. Some of the key solutions are listed below:

- Diversify Funding Sources: FSPs should explore various funding sources beyond external debt, such as seeking investments from impact investors or philanthropic organisations that are aligned with the mission of serving MSEs. FSPs should encourage more savings and deposits as a source of capital to sustain and grow their loan books.

- Risk Mitigation Strategies: Implement robust risk assessment and monitoring systems beyond KYC to better understand the creditworthiness of MSE borrowers. This may include data analytics, alternative credit scoring models, and cash flow analysis.

- Consider group lending models that leverage social security and credit ratings within the MSE community to minimise individual borrower risk.

- Credit Information Sharing: Encourage the adoption of credit reference services in collaboration with other FSPs. Sharing credit data across institutions can help reduce the risk associated with MSE lending and improve the creditworthiness assessment of borrowers.

- Digital Solutions: Invest in digital infrastructure and mobile banking technologies to enhance outreach and provide convenient and cost-effective financial services to dispersed MSEs without access to conventional brick-and-mortar financial service stations.

- Community Engagement to enable product design and diversification: Continue to collaborate with the communities to design financial products and services that are more aligned with the specific demands of MSEs.

- Impact Measurement and Reporting: Regularly assess the social and economic impact of MSE financing to demonstrate the value of serving this sector to investors, donors and regulators.

- Use the performance data to fine-tune and improve financial products and services for MSEs.

Conclusion

The primary hurdle impeding the financing of the MSE sector lies in the formidable challenge of entrepreneurs being unable to fulfil the stringent criteria established by financial stakeholders. This critical barrier obstructs the sector’s growth and calls for affirmative action that addresses the unique financial needs and limitations of MSEs, fostering a more inclusive and supportive financial landscape for aspiring individuals and small businesses alike in Uganda.

This insight is not paid research but rather internal research based on our advisory and data projects. It is being shared to create public debate and, as such, we welcome any suggestions for improvement. Kindly contact us at info@asigmacapital.com