Overview

As Uganda targets to achieve upper middle-income status by 2040, non-fuel minerals have been identified as strategically important in key strategy documents including Uganda’s Vision 2040 and the third National Development Plan (NDP III). Both strategy documents identify mining and mineral beneficiation as a critical subsector in delivering Uganda’s resource-based industrialisation and job creation agenda.

Uganda’s mineral sector is a large contributor to export earnings with sectoral contributions to export earnings averaging at US$ 799 Million, between 2o16 and 2020, and growing at a compound annual growth rate (CAGR) of 36%.

The Mining Sector’s Contribution to Uganda’s Economy

The contribution of the mining and quarrying sector to Uganda’s GDP has been growing by a CAGR of 19.7% over the five-year period ending FY 2018/19. This growth is attributed to increased political stability and friendly investment policies such as the Minerals Policy (2018), and the Mining Act (2003) and the Mining Regulations (2004). Additionally, financial support from development organisations such as the World Bank Group, African Development Bank, Nordic Development Bank, Geological Survey of Finland etc. has also contributed to the growth of the minerals sector in Uganda by way of policy formulation, geochemical surveys and mapping as well as capacity building.

Furthermore, Uganda’s mineral sector is a large contributor to export earnings with sectoral contributions to export earnings between FY 2015/16 and 2019/20 averaging US$ 799 million and growing at a CAGR of 36%. The exports from FY 2018/19 upwards are due to the establishment of the African Gold Refinery (AGR). As at 2019, gold is Uganda’s largest contributor to export earnings accounting for US$ 528 million and growing at a CAGR of 53% over the five-year period ending FY 2019/20.

Mineral Occurrences in Uganda

Uganda possesses a rich and highly diverse mineral resource base owing to her position within the Western Rift as well as its proximity and geological similarity to resource-rich DRC.

[display-map id=’3538′]

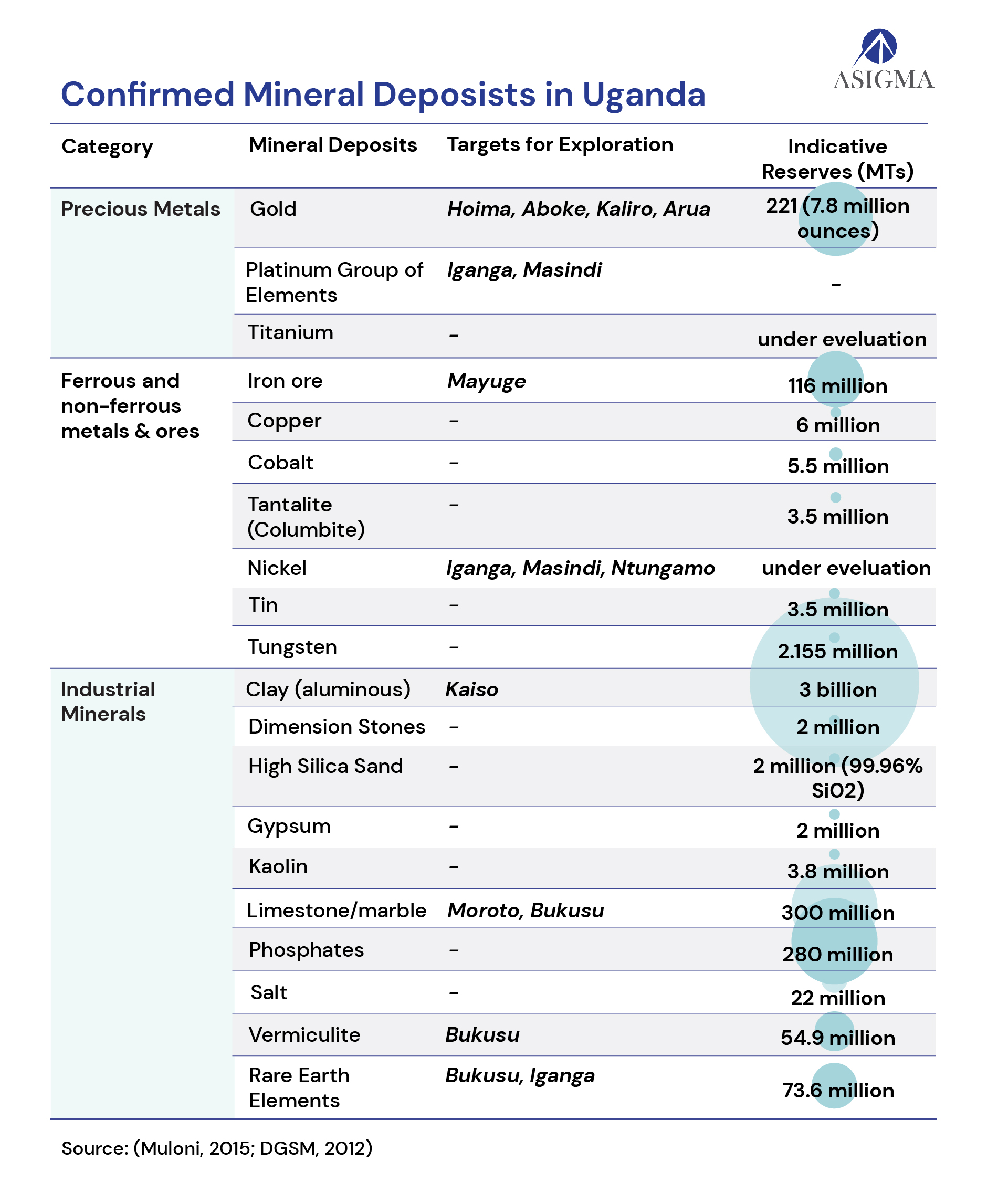

Confirmed Deposits

Uganda’s mineral resources such as gold, copper, iron, 3Ts and an assortment of development minerals such as apatite, commercial beryl, emerald and aquamarine have attracted an increased FDI within the mining and mineral beneficiation sector from USD 5 Million in 2003 to over USD 800 Million in 2017.

Due to this, the Government of Uganda and its development partners have invested significant resources in mineral exploration activities including geophysical and geochemical surveys and mapping to determine the existence, location and quantities of Uganda’s mineral resource base. The table shows the estimated reserves of select minerals in Uganda.

Uganda as a Mining and Mineral Beneficiation Destination

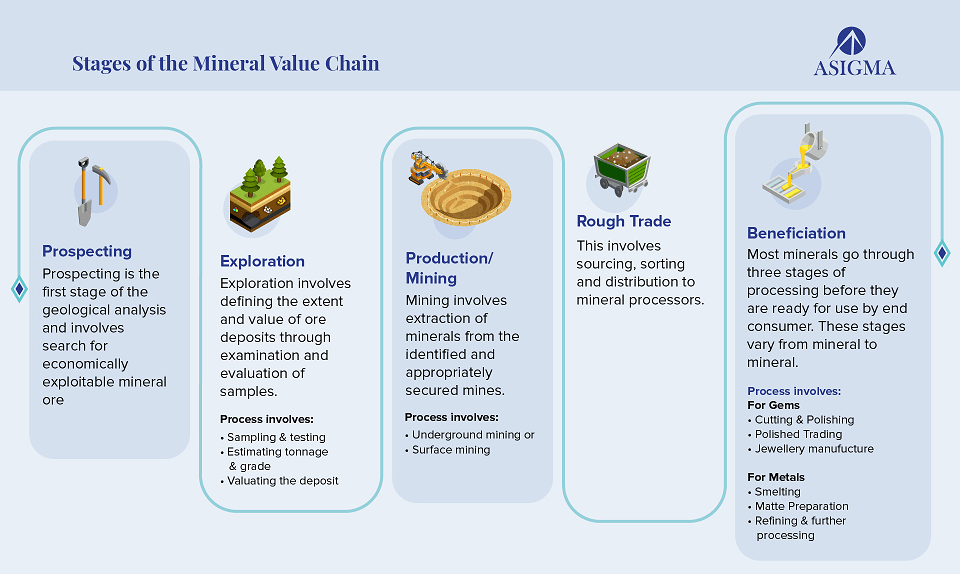

Opportunities exist in the minerals sector across most commodity value-chains, i.e., from prospecting and exploration to mining and production through to beneficiation and value addition. Given the price and margin trends within the ferrous and non-ferrous metals category, favourability for large-scale mining activities based on prospective returns is predominantly in iron ore, nickel, copper and cobalt. In the precious metal category, margins for gold and silver are also attractive and likely to attract significant investor interest.

The government requires that minerals mined in Uganda should be processed and refined in Uganda into semi-finished or finished products before they are exported. Currently, copper, cobalt, lithium, graphite and iron ore are strictly not for export in raw form; the rest can be exported as high concentrates.

The table below highlights the different investment opportunities within the key minerals across the value-chain in the Ugandan market.

Policy and Incentives Regime

In accordance with the National Development Plan (NDP III), the Ugandan government is committed to the development of the mining sector and has provided the following incentives to attract investors into this sector.

Legal, Regulatory and Institutional Framework

The Government of Uganda through the Ministry of Energy and Mineral Development drafted the Mining and Mineral Bill, 2019. The Bill seeks to consolidate and reform the Law relating to Mineral resources to give effect to article 244 of the constitution. It also seeks to repeal the outdated Mining Act, 2003 and provide for administrative and institutional reforms for better governance and management of the Mining sector.

The Draft Minerals and Mining Bill 2019 proposes that in addition to being a regulator and guarantor of mineral rights, the State will become a participant in mining projects undertaken by private investors through a national mining company to be established under the Companies Act. Below are the mineral licences and permits available to actors.

Uganda’s Mining Sector Players

Uganda has enjoyed a favourable business climate over the last decades, that has enabled the development of the mining sector and attracted several players as highlighted below.

Exploration

The commodity-focus of recent exploration activity has been copper, cobalt, nickel, and other ferrous and non-ferrous metals as well as gold, with global market variables, such as demand and price driving the focus. Regardless, prospecting and exploration activities are limited to a few large players, specifically junior mining companies, mid-tier mining companies and a host of others Ugandan or foreign venture-capital funded mining companies running small scale operations.

Major junior mining companies engaged in exploration activities in Uganda include Sipa Exploration Uganda, a subsidiary of Australian Sipa Resources, and Jervois Mining with its parent company based in Australia. Sipa’s interests are in the Kitgum-Pader Base Metal Project while Jervois’ interests are in Kilembe and Bujjagali in West and Central Uganda, with the company resuming diamond drilling in 2019 with non-ferrous metals-copper, cobalt, and nickel.

Most junior miners have entered joint ventures with other junior and large mining companies. Examples of these include African Panther Resources which entered a partnership with Australian junior miner, Carnavale Resources, in the early-stage Kikagati tin project, while junior explorer, Sipa Exploration Uganda, partnered with large miner Rio Tinto in the North copper-gold project. Both multinationals have since exited their interests in Uganda. Carnavale’s 2019 exit from a 70% option to acquire the project was due to lack of commercial viability of the ores for economic development amid falling tin prices. The reasons for Rio Tinto’s 2020 exit from the earn-in and joint venture after spending US$ 4.2 million in diamond drilling, round gravity and ground magnetic surveys are yet to be publicly disclosed.

Minerals Beneficiation

It is important to note that companies in possession of mining or mineral dealer licences or otherwise engaged in first or second-stage mineral beneficiation are also engaged in prospecting and exploration activities. This is predominantly with the intent to extend the mine life of existing interests through the discovery of additional reserves (brownfields) or identify locations for greenfield development. The intent for actors engaged in beneficiation activities looking to expand into exploration and mining activities is to integrate and domesticate supply chains and secure feedstocks for their manufacturing.

Below are some of the players and activities in the beneficiation of gold, iron, copper- cobalt and the 3Ts.

Gold: Goldsmithing licences have been limited to first-stage processing by gold refineries. The entry of AGR into in-country gold value addition together with Bullion and Simba gold refineries has been vital in ramping up production upstream, especially by artisanal and small scale miners (ASMs) who primarily rely on direct or brokered relationships with in-country refineries, or large traders (bulkers and aggregators. The reliance of existing refineries on both in-country ASM sourcing and regional sourcing of gold ore or doré, specifically from the DRC and South Sudan, is indicative of Uganda’s emerging position as a regional gold processing and trading hub. At present, there are no known third-stage gold value addition activities in Uganda in the form of jewellers or manufacturers of gold items with applications in dentistry.

Iron: Several parties in particular steel processing plants with in-country operations have expressed interest in engaging in iron ore mining as well as smelting as part of their vertical integration strategies. Among these is Roofing’s Rolling Mill which is looking to engage in mining activities as well as establish an iron ore processing plant that requires a capital base of between US $300 million and $1 billion. Tembo Steel also intends to mine iron ore in the East as well as establish a steel mill with an envisaged capacity of 500,000-600,000 MT/year. Both investments are targeting the East African market.

Copper-Cobalt: Ministry of Finance, Justice, Energy and Kilembe Mines Limited were mean to fast-track the process of identifying a new investor to revamp the mines after termination of a concession agreement with Tibet Hima Mining Company in 2015. It is said that, once a major copper and cobalt producer, the Kilembe Copper Mines was last managed by a Canadian firm – Falconbridge that exited Uganda in the 1970s at a time when output is said to have peaked.

Tin, Tungsten and Tantalum (3Ts): Production of the 3Ts has been marginal in terms of volumes and has been dominated by 3T Mining and Krone Uganda (now suspended). There is however significant artisanal and small-scale mining activity, specifically in the Southwest. Within the tin value chain, ZANACK holdings operational in Mwerasandu is a major player in tin mining. As part of its beneficiation agenda, GoU has in place plans to set up a centralised processing plant for concertation of tin in Ntungamo in the West that will source from the Mwerasandu Tin Mining Site.

Supporting Functions

There are several players providing infrastructure support, capacity building, financing, research and development, machinery and equipment supply among others as briefly explored below.

1. Infrastructure Provision: Mining projects require large infrastructure support to extract product and transport it to its final destination. This infrastructure includes but is not limited to roads or rail transportation, water systems, power, telecommunications among others.

Mining consumes a lot of electricity and the major challenge to people in the extraction process is the lack of three-phase power. To create a reliable power supply, big mines such as Kilembe mines have set up their own power plants and the surplus is sold to the national grid. Small players however rely on generators that increase the cost of operation.

Regarding water access system, reliable supply of water is important for mining and mineral processing because the processes involved consume significant volumes of water. National Water and Sewerage Corporation was set up to serve urban areas of Kampala, Entebbe and Jinja but is now serving more than 250 towns within the country. For remote areas outside NWSC influence, Rural Water Supply and Sanitation Department (RWSSD) under the Directorate of Water Development in the Ministry of Water and Environment is responsible for the provision of safe water and sanitation services in rural areas across the country.

2. Machinery and Equipment Supply: There is a presence of suppliers and service providers of machinery and equipment with applications in exploration and mining in Uganda such as drilling (breakers, demolition tools and drills), earth moving equipment, compression and compaction and tipper trucks for transportation etc. Major suppliers of exploration and mining equipment in Uganda include ADT Africa and Supercore that serve SIPA Resources Ltd. Other notable actors include Norjo Construction and Mining Techniques. These actors source equipment from mainly China and provide specialised service and machinery leasing models to their clientele.

There is no evidence of the presence of suppliers of smelting machinery specifically for value chains with in-country value addition being gold and tantalum. Sourcing of machinery is predominantly external. Major global suppliers include APT in South Africa and Changfa in China. Other major global suppliers include the Nile Company, JSXCS, Falcon Concentrators, Nelson Concentrators and Holan among others.

3. Financing: Availability of financial services to the mining sector is dependent on the scale of mining. At the artisanal and small-scale mining (ASM) level, financing is usually through informal channels with individual benefactors financing the activities of a group of ASMs. Formal finance to ASMs is limited primarily due to the high-risk profile of actors engaged in mining. However, a few in-country commercial banks are responding to the financing gap by deploying ASM targeted facilities. Stanbic Bank for instance launched a business incubator fund in 2019 targeted at Small and Medium-Sized Enterprises (SMEs) across all sectors including mining.

Larger actors rely on concessionary financing from concessionary lenders such as the China Exim Bank. While not actively engaged in the sector, local and regional Development Finance Institutions (DFIs) with the capacity to finance large scale mining investments include World Bank’s International Finance Corporation (IFC), the East African Development Bank (EADB) and Uganda Development Bank (UDB).

4. Insurance: This is largely in the form of Political Risk Insurance (PRI) targeted at investors with interests in developing economies characterised by high political risk such as Uganda. The World Bank’s Multilateral Investment Guarantee Agency (MIGA) has been most active in advancing PRI to Ugandan mining projects. MIGA provides mining investments with cover against non-commercial risks. These include the risk of “currency inconvertibility and transfer restrictions, expropriation, war and civil disturbance and breach of contract”. In 1998, MIGA advanced a guarantee to Canadian and French Banff Resources Ltd and LaSourceSAS for interests in the Kasese Cobalt Company Ltd. Consortium.

5. Research and Development: Research and development activities within the mining and mial beneficiation sector fall broadly within two categories that is acquisition and dissemination of geological data, as well as provision of analytical laboratory services. DGSM is responsible for both functions. DGSM’s Geological Survey Department (GSD) is responsible for carrying out mineral exploration activities as well as generating and disseminating geological information through the integrated management information system, online mining cadastre system that can be accessed through their website.

Furthermore, DGSM possesses a central analytical laboratory offering “geological material sample preparation, chemical analysis, ore test work, technical advisory services and training as part of the geological data and inspection, monitoring and regulation of the mineral exploration, mining and mineral trade activities.

There are also a host of secondary analytical laboratories that include Uganda Industrial Research Institute (UIRI), AGR, Uganda National Bureau of Standards (UNBS), Ministry of Works and Transport’s Construction Standards and Quality Assurance Department Central Materials Laboratory, and Hima Cement Plant lab. Given the limited in-country analytical lab capacity, entities involved in prospecting and exploration activities typically ship off samples from Uganda to analytical labs in Australia, South Africa, and the UK for testing.

6. Training and Capacity Building: Generally, the supply of training institutions for skilling mining professionals with expertise in geological studies, mining engineering, physical metallurgy, environmental science and analytical chemistry remains limited. Although this is little to no targeted sector-specific skilling, Vocational Training Institutions in Uganda such as Nakawa Vocational Training Institute, Ntinda Vocational Training Institute exist that train electricians, boiler makers, welders etc whose skills are relevant to the mining sector. A few specialised schools and programs have risen, as the country gears for oil drilling, that are offering international certifications for artisan type jobs such as Uganda Petroleum Institute – Kigumba and Nile Vocational Institute Bishop Mukasa Centre among others.

All this culminates from the nascent nature of Uganda’s mining sector which presents limited specialised training institutions and limited opportunities for hands-on skilling and learning through industrial training and internship placements.

7. Collective Arrangements: The Uganda Chamber of Mines and Petroleum (UCMP) represents the interests of private players in the mining and petroleum sectors in Uganda. UCMP collaborates with the state to develop the country’s extractive sector. To further facilitate greater networking and collaboration in the country’s extractives sector, in partnership with MEMD, UCMP is the organiser of the annual Mineral Wealth Conference (MWC) which brings together key policy and decision-makers, business leaders, bankers, academia and mining investors from all over the world.

In Uganda, artisanal and small-scale mining (ASM) players are loosely formed into networks and associations that are intended to collaborate to address their cross-cutting issues such as market, raw material sourcing, technical capacity building, access to finance, technology and markets. In Uganda, the most prominent arrangements are National Artisanal and Small-Scale Miners Association (NAMSA) and District Artisanal and Small-Scale Miners Association (DAMSA) in 17 strategic mining areas in Uganda both of which are dormant as well as an assortment of fragmented ASM groups such as Syanyonja Artisan Miners Alliance (SAMA) in Busia.

In 2016, SAMA began the first gold mining cooperative in Africa to become Fairtrade certified. Actors like UNDP, Fairphone and others are working with ASM collectives to support their formalisation and business acceleration initiatives, strengthen environmental and social safeguards as well as gender and capacity gaps. Another key mining sector development is the ongoing ASM miners, which currently make up almost all of the country’s total domestic production pioneered by Government.