Key insights from the 2023 finscope study

July 17, 2024

About the 2023 FinScope Study

The 2023 FinScope survey was a demand-side study of access, uptake, usage and perceptions of financial services in Uganda. The main objectives of the study included:

- Track Financial Inclusion Trends: Assess changes in financial inclusion since 2018 and benchmark these trends with other countries in the region.

- Provide Policy and Market Insights: Offer data-driven insights to deepen financial inclusion at both policy and market levels.

- Describe Financial Service Needs: Identify the financial service needs of adults (16 years and older) in Uganda.

The findings from this survey then assist financial sector stakeholders in developing and delivering services to lower-income households and creating an enabling environment for these services.

Insights from the Study

1. Increased Demand for Financial Services

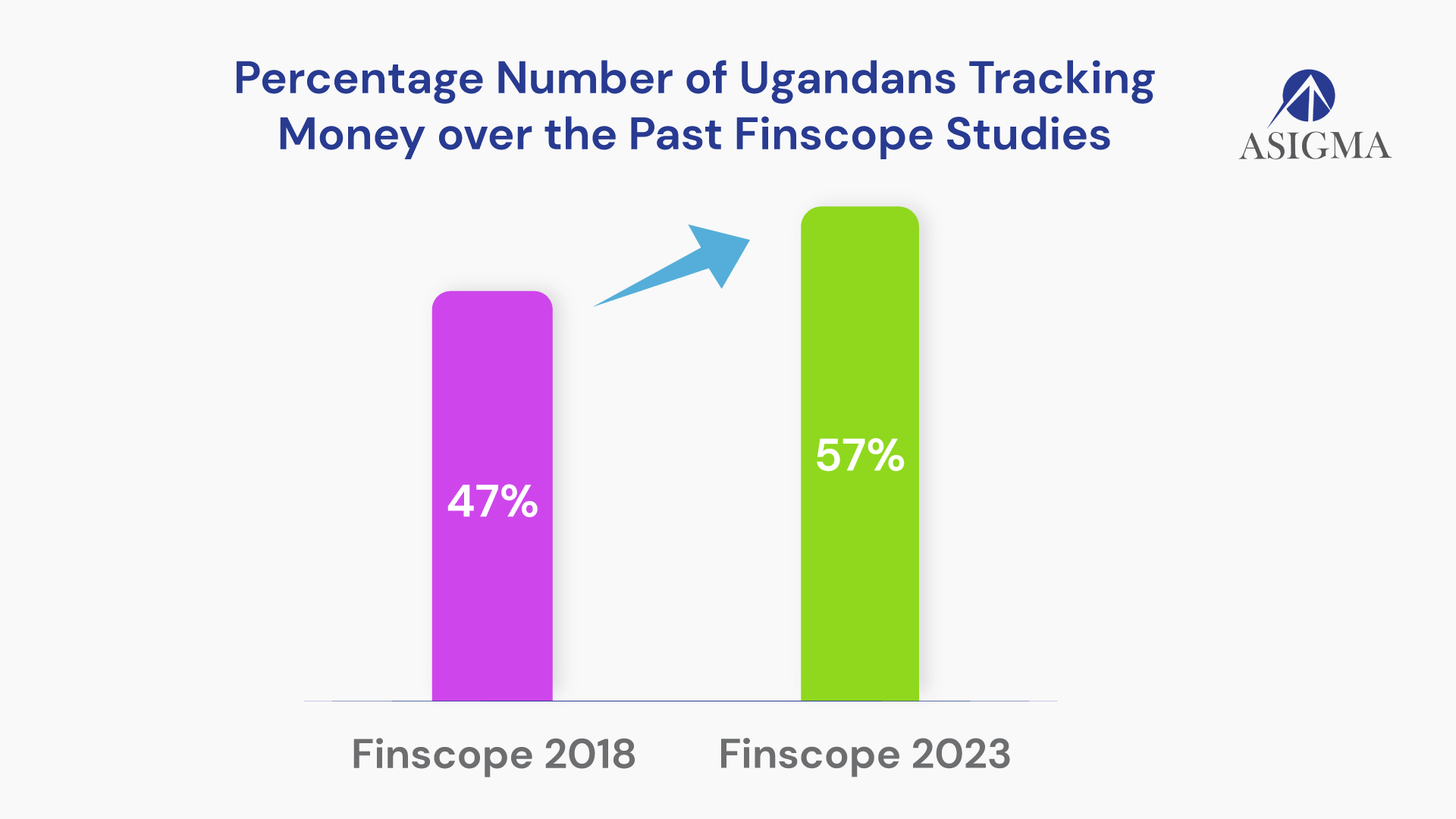

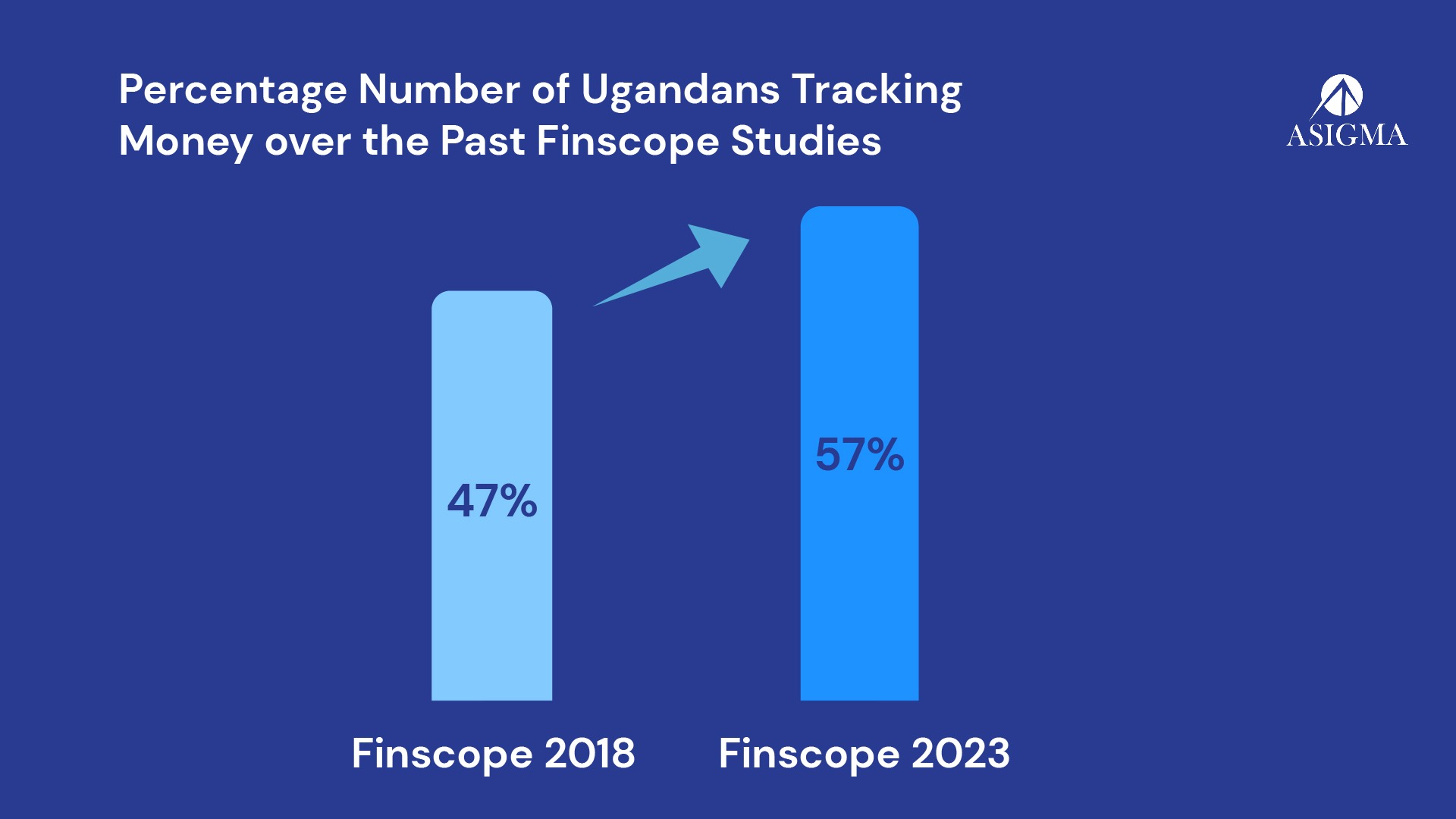

The proportion of Ugandans who keep track of the money they receive and spend has increased by 10% from the previous FinScope (2018) as shown in the graph below:

This implies that more Ugandans can keep track of their financial records and can therefore track their current/future debt obligations hence the ability to avoid any penalties that come with late repayments of debt. Some of the key drivers for this growth are increased smartphone usage, financial literacy and access to mobile money services.

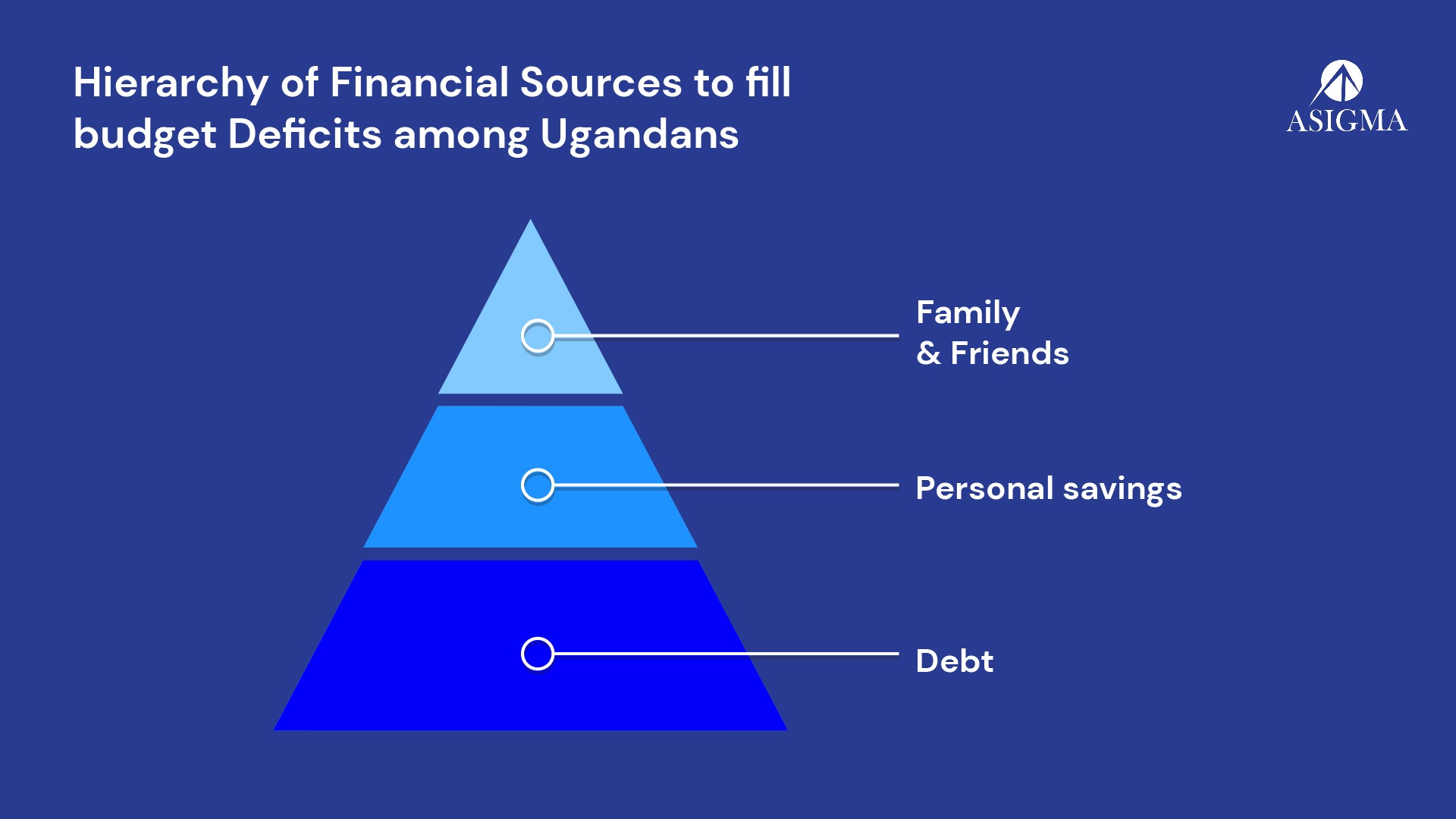

Seven (7) out of every ten (10) Ugandans are operating with a personal budget deficit highlighting the need for more money than they are earning to cover their personal financial needs. Because of this, Ugandans are relying on their family and friends, personal savings before considering debt to manage their budget deficits. According to UBA x ASIGMA Digital Lending Article Series I this is attributable to the fact that these options are cheaper and more accessible, and that there is a general fear for acquiring debt. This further implies that there is a need for FIs to innovate and tailor loan products that solve these barriers and meet the unique consumptive needs.

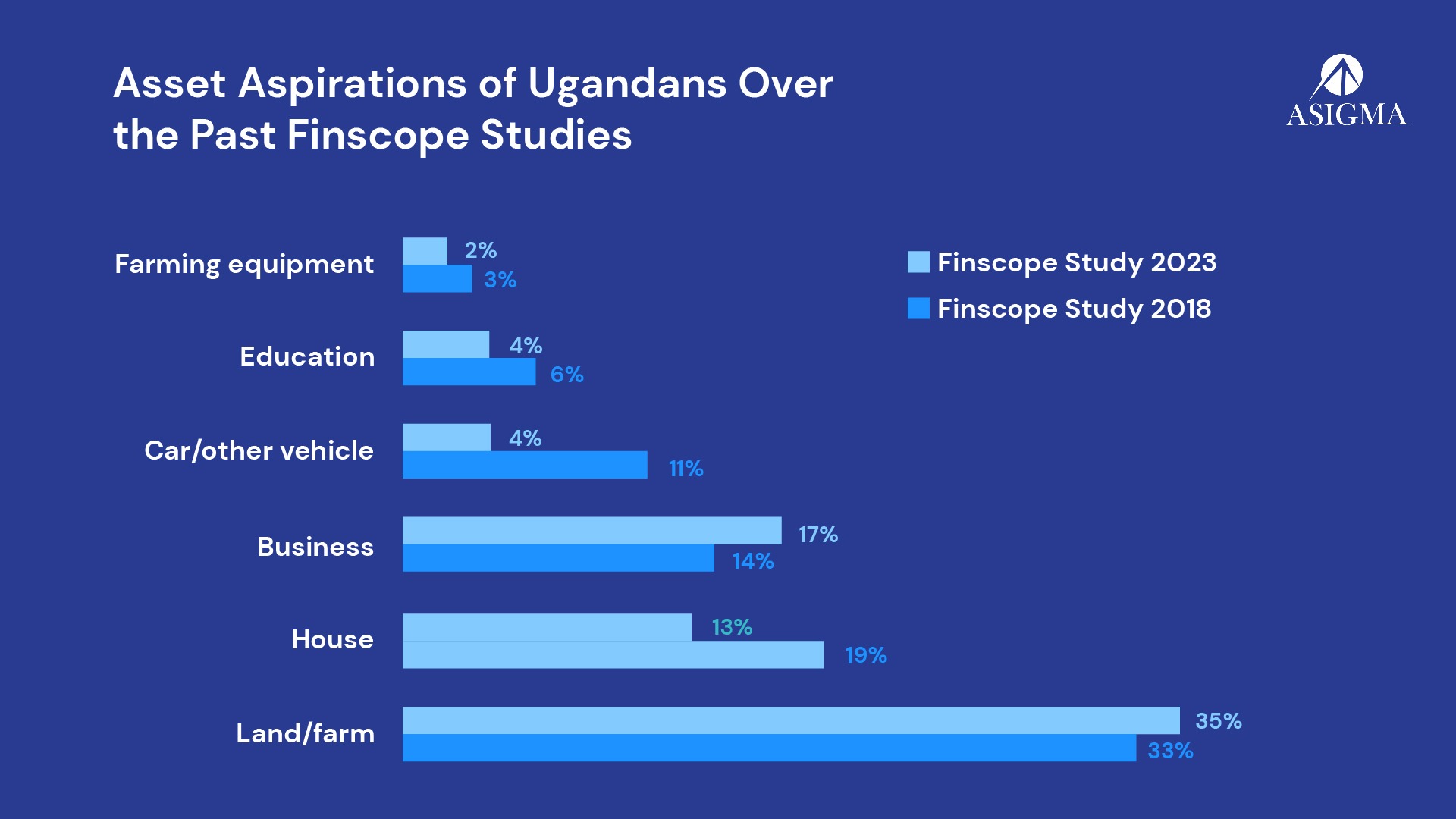

Purchase of land, farming and running a business continue to be the predominant investment aspirations for Ugandans as shown in the graph below:

There is more demand for financial products tailored to asset financing, agriculture, as well as business respectively.

2. Digital Lending, a bridge to financial services

Below are some of the reasons why digital lending through FinTechs and MNOs is a bridge to financial services:

FinTechs unlike most traditional financial institutions can leverage transaction data and other alternative data sources for analytics to inform credit product pricing hence a risk-based form of pricing as opposed to the traditional flat pricing which is sometimes prohibitive and exclusive.

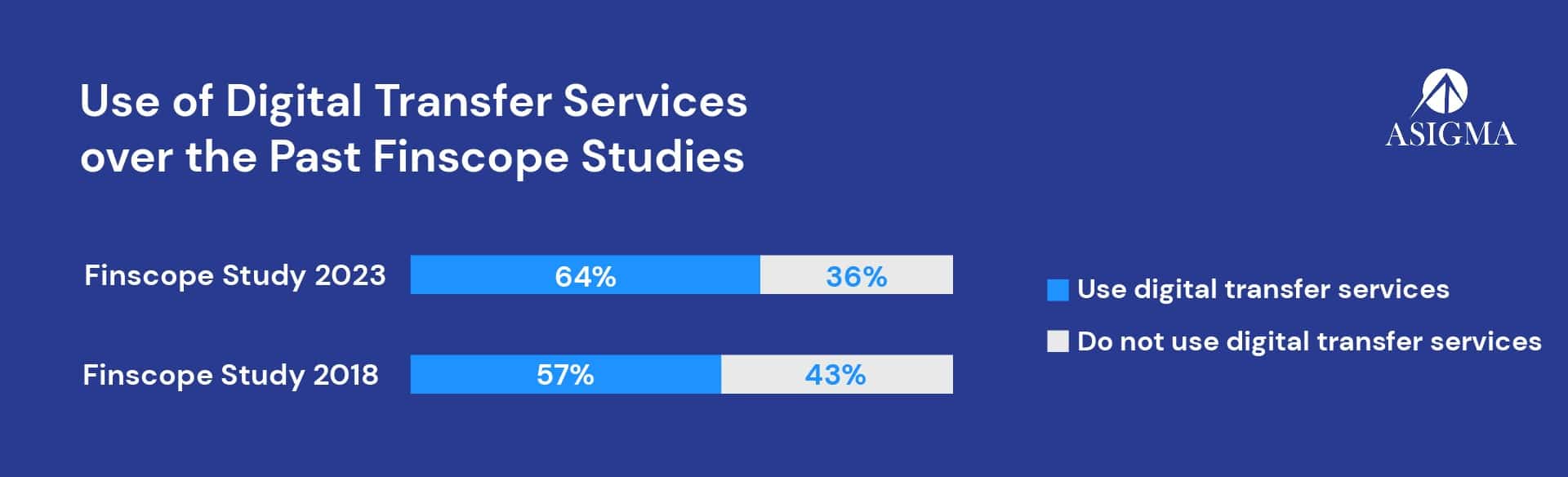

This is partly evidenced by the statistics from the FinScope Survey that indicate that the proportion of Ugandans using digital transfers (which are an enabler of digital credit) has slightly increased since 2018 from 57% to 64% as shown on the graph. It is however important to highlight that the increased uptake of digital services is majorly due to their ease of accessibility.

FinTechs create a platform for collaboration and easy integration with other online actors such as the digital marketplaces such as Mobile Network Operators (MNOs) to offer credit to both the demand and supply side in what is referred to as embedded digital finance. The FinScope Study shows that mobile money continues to be the predominant formal source of credit.

FinTechs ease the accessibility of finance by significantly reducing the loan processing period from days to minutes or even seconds thereby fostering access to finance. The statistics from the study indicate that formal inclusion continues to be driven by mobile transactions.

3. Digital Connectivity and Financial Eligibility

The survey highlights a rise in mobile phone ownership, yet it also underscores the persistent disparities. These disparities are evident between urban and rural regions, as well as between genders. The situation is further complicated by the widespread lack of proof of residence, a requirement that many Ugandans find challenging to meet for financial eligibility. This digital divide, coupled with the absence of residential proof, hampers financial inclusion efforts, especially among rural communities and women.

Furthermore, formal inclusion is higher amongst men and urban dwellers while Informal inclusion is higher amongst women and rural dwellers. This is attributed to the fact that women and rural dwellers prefer to access credit through informal institutions such as SACCOs and VSLAs which offer loan products that are tailored to their needs, not collateral restrictive, and offered to a group of individuals.

4. Green Financing

Only 28% of Ugandans are aware of green growth concepts, with only 11% aware of green finance. High poverty levels and lack of awareness hinder green growth. This low awareness has the potential to significantly hinder the adoption of sustainable practices in the country.

Call to Action for Different Stakeholders

1. Government and Policy Makers

- Financial Literacy Programs: Implement nationwide financial literacy programs to educate the population on budgeting and financial planning which in turn enables citizens keep track of their financial obligations.

- Green Finance Initiatives: Enhance awareness and facilitate access to green finance to support sustainable practices and climate resilience.

2. Mobile Network Operators (MNOs) and Financial Service Providers (FSPs)

- Digital Infrastructure: Invest in expanding digital infrastructure to rural areas to enhance connectivity and access to digital credit.

3. Financial Institutions (FIs)

- Inclusive Financial Products: Develop financial products that cater to the needs of lower-income households and informal workers as well as small traders and service providers. This could be through leveraging emerging technologies like artificial intelligence and machine learning to develop innovative financial products that address the specific needs of different demographic groups, including women and rural populations. This would perfectly aligned with the National Financial Inclusion Strategy (2023 – 2028) that seeks to incentivize and place a particular focus on uplifting the marginalized.

- Digital Financial Services: Expand digital financial services, particularly in rural areas, to bridge the connectivity gap and promote formal financial inclusion in these areas.

- Risk-based pricing: Financial Institutions are implored to double down on risk-based pricing to foster more financial inclusion in the country.

4. Development Partners and NGOs

- Capacity Building: Invest in financial literacy programs to educate the population on financial planning, budgeting, and the benefits of formal financial services.

- Support Green Growth: Partner with local institutions to promote green finance and sustainable agricultural practices.