The race to meet Bank of Uganda’s new capital requirements approaches tail end

June 20, 2024

Unveiling the Dynamics Behind Uganda’s Regulatory Shift in Banking Capitalisation

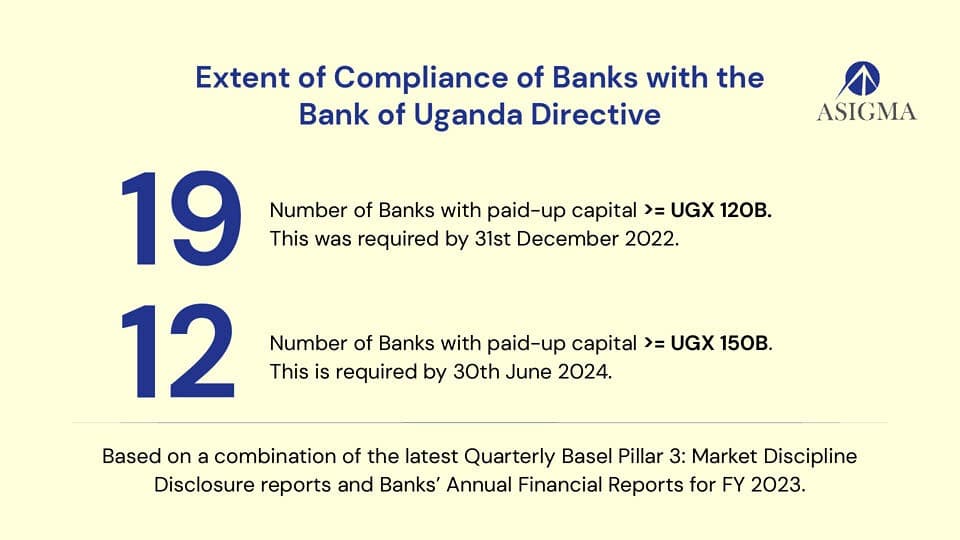

In 2022, the Bank of Uganda (BOU) proposed increasing the minimum paid-up capital requirements for major financial institutions operating in Uganda. After consultations with relevant stakeholders, BOU increased the minimum paid-up capital requirements, and all financial institutions were given a deadline of 30th June 2024 to comply. The minimum paid-up capital requirement for commercial banks (Tier I financial institutions) was increased from UGX 25 billion to UGX 120 billion by 31st December 2023 and UGX 150 billion by 30th June 2024. Concurrently, BOU raised the minimum cash reserve requirement from 8% to 10% of total deposits for commercial banks. These reforms reflect BOU’s strategy to fortify financial stability, enhance risk management frameworks, bolster market competitiveness, align with international standards, and mitigate systemic risks.

Compared with international standards such as Basel III, which are recommendations on banking regulations issued by the Basel Committee on Banking Supervision in response to the financial crisis of 2007–2008, BOU’s decision is a step in the right direction. Basel III sets international standards for banks’ capital adequacy, leverage, and liquidity requirements. Basel III recommends banks to maintain common equity of at least 4.5% of their risk-weighted assets and a leverage ratio of at least 3%. Hence, increasing paid-up capital requirements is a step in improving capital adequacy and leverage for banks to meet recommended global standards.

In this analysis, we delve into the underlying drivers and implications of these regulatory reforms, offering insights into the future trajectory of Tier 1 banks and the broader financial ecosystem.

Navigating Change

Strategies and Challenges in Meeting BOU’s New Capital Requirements

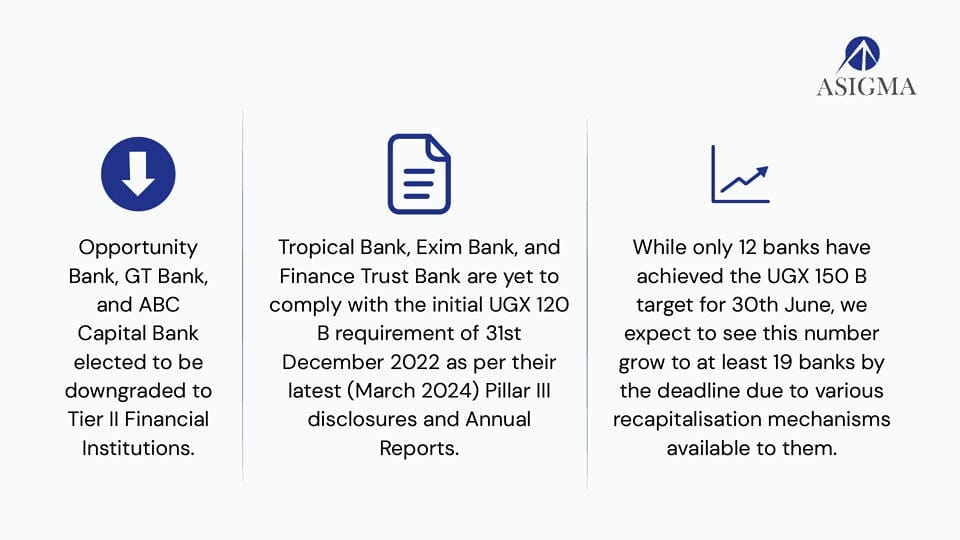

To meet BOU’s new requirements, different banks adopted different strategies. These include merger & acquisition initiatives with larger international banks (Nigeria’s Access Holdings will acquire an 80 percent stake in Uganda’s Finance Trust Bank Ltd in a transaction that is expected to be closed in the first half of this year), issuing additional shares and downgrading their banking licenses from Tier I to Tier II. The banks that have applied to downgrade are Guarantee Trust (GT) Bank, ABC Capital Bank and Opportunity Bank.

Exploring the Macroeconomic Effects of the Increased Paid-Up Capital Requirements

The increase in minimum paid-up capital requirements for banks will increase the resilience and ability of the banks to absorb any shocks in the economy. These shocks may arise from global or local financial crises, economic downturns, extended recessionary periods, and geopolitical events. A higher minimum paid-up capital and an increase in the minimum cash reserve (amount of customer deposits kept by banks in cash or near cash assets) will build a stronger financial sector that can easily meet liquidity needs in times of crisis.

The increase in the minimum cash reserve requirements will reduce the growth of broad money (M2) in the economy which will reduce inflationary pressures. This will mainly be achieved through the reduced money supply in the economy, which will hinder the growth in purchasing power and ultimately inflation. However, BOU is actively deploying other strategies such as increasing the Central Bank Rate and other Open Market Operations to control the inflationary environment in the Ugandan economy.

Despite the benefits of increasing the minimum paid-up capital requirements such as financial stability for banks and increased customer confidence in local banks, there are also some key negatives to note.

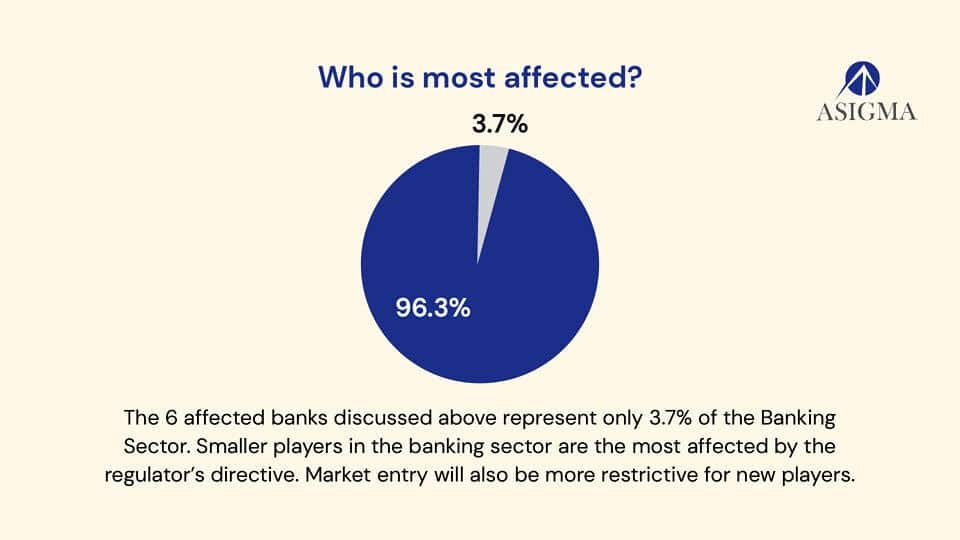

The increase in the minimum paid-up capital requirements will negatively impact the already low financial inclusion in Uganda. Commercial banks like Opportunity Bank with crucial financial inclusion operations in Karamoja are downgrading to credit institutions. This means that financial services and products offered in such regions will be lowered. Larger commercial banks that have met BOU’s increased requirements tend to prioritise less risky, well-established clients.

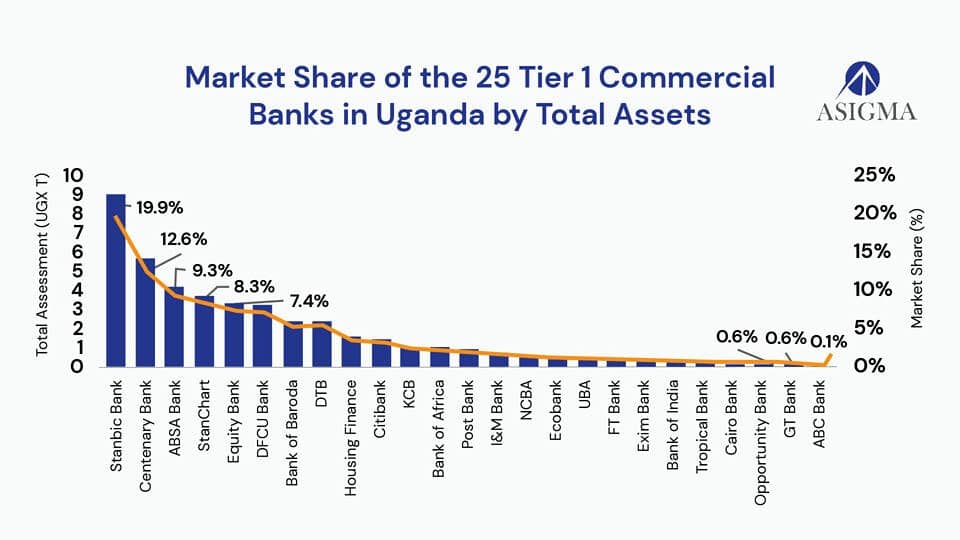

Current Position within the Market

This analysis provides insights into how different institutions are positioned within the market and how they may be impacted by regulatory changes.

Stanbic is the clear market leader in terms of total banking assets relative to the rest of the industry actors.

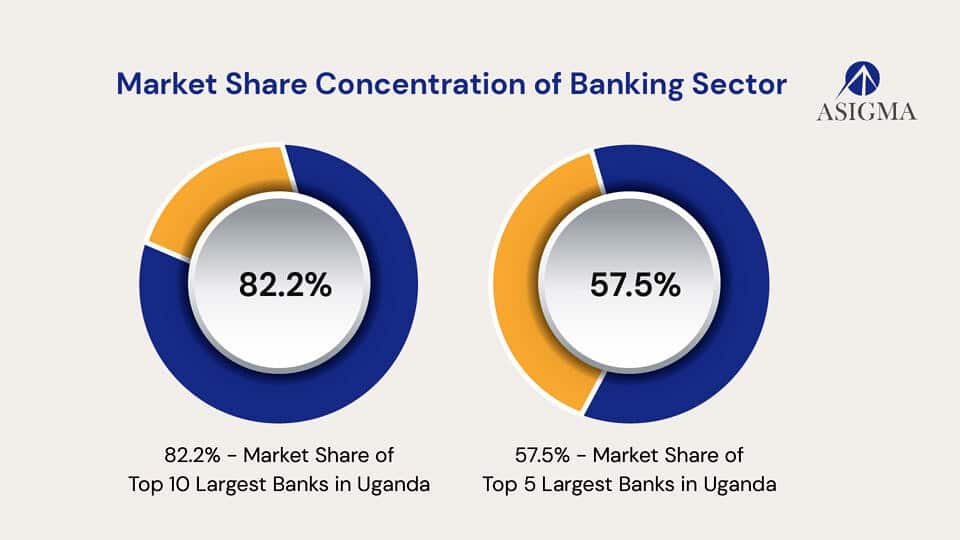

“By comparison, Uganda’s banking sector is more competitive than South Africa’s, with a diverse range of players contributing to the market. In South Africa, the top 5 banks dominate over 80% of the market share.”

Where do the banks currently stand?

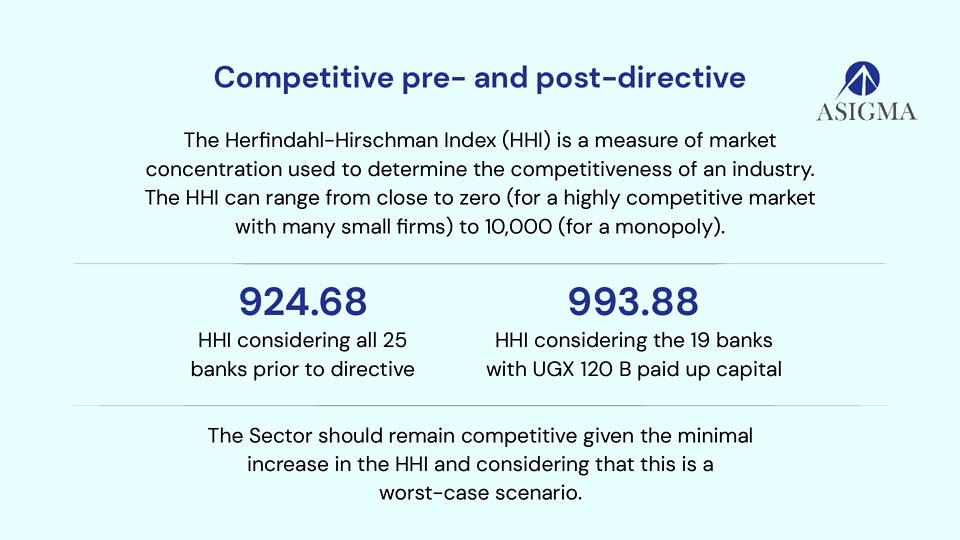

Given the confirmed downgrading of three (3) banks to a lower tier, concerns about the impact on the existing level of competition within the sector arise. We explore this using the HHI analysis below.

With the expected mergers and acquisitions coupled with the downgrade of some commercial banks, the number of institutions in the commercial banking space has reduced. This reduces competition which may eliminate the incentive of the banks to offer competitive rates and fees to Ugandans.

Exim Bank Uganda’s compliance could not be verified as their relevant reports were inaccessible. Latest status on non-compliance is available here.

Case Studies

Stanbic Bank Uganda Limited (SBU)

SBU is the largest bank in Uganda and one of the banks that has met the new minimum paid-up capital requirements before the deadline. To meet the requirements, SBU issued 102,377,339,000 additional ordinary shares in 2022 which were paid using the already existing share premium in the banks’ equity. This means SBU did not have to raise any external funds, and the BOU’s regulation did not affect the bank’s total equity. However, the equity structure changed since the share premium in 2022 was reduced by UGX 104 billion and the paid-up share capital was increased by UGX 102 billion to meet BOU’s regulations. This means BOU’s new regulation didn’t affect SBU’s operations.

Guarantee Trust Bank (GT Bank), ABC Capital Bank and Opportunity Bank

As of April 2024, GT Bank, ABC Capital Bank and Opportunity Bank had applied to BOU to downgrade their banking licenses from Tier I to Tier II. These banks are now in the process of reducing the scale of their operations and phasing out some of their current service offerings that are limited to Tier I financial institutions.

Unlike Tier I financial institutions, Tier II financial institutions cannot operate checking accounts or trade in foreign exchange. Checking accounts are bank accounts where funds can easily be accessed through electronic transfers, ATM/debit cards and checks and are mostly used by retail banking customers. Scaling down operations to a Tier II financial institution means the three banks will focus on their business and corporate clients and miss out on the retail customer market segment.

Additionally, the restriction on foreign exchange trade will affect the revenues earned by the banks that are scaling down to Tier II. An example is GT Bank, whose earnings from foreign exchange trade contributed 13% and 9% to the bank’s total revenue in 2021 and 2022 respectively. That highlights GT Bank’s potential revenue loss in the following financial years.

Conclusion

BOU’s new requirements are a critical component of financial regulation aimed at promoting stability, resilience, and responsible banking practices. A well-capitalised banking sector is better positioned to withstand economic shocks and disruptions, thereby safeguarding the broader economy. However, this could come at the risk of reducing competition among the top commercial banks since some institutions have been forced to downgrade their licenses or exit the market.